Last updated: 25 Aug 2025 09:00 Posted in: AIA

The benefits of a stepwise framework for responsibly integrating AI into the accounting profession, by Dr Tim V. Eaton, Dr James Zhang and Alexa Leach.

Generative artificial intelligence (AI) has captivated the accounting profession with its potential to create unforeseen growth in effectiveness and efficiency. While AI is already impacting the profession in both public and private accounting organisations, it is incredibly important to fully consider and properly manage the benefits and risks of this technology. Things are moving fast. We draw a simple parallel between AI innovation and the concept of ‘warp speed’ (the technology in the popular Star Trek series that allows interstellar travel with maximum efficiency!).

More recently, the concept of warp speed was used by the United States government in the incredibly rapid development of the Covid-19 vaccine through Operation Warp Speed, which included the necessary oversight and mobilised the appropriate resources to deliver, produce and distribute vaccines effectively.

Similarly, the use of AI in accounting will require organisations to establish clear frameworks and levels of oversight to maintain growth and competitiveness. The mobilisation of resources in Operation Warp Speed can be compared to employee knowledge, as accountants will need to be educated on the proper use of AI. Just as the US needed to adapt to Covid-19 rapidly, the accounting profession must implement this technology to maintain relevance. However, it must be implemented responsibly to demonstrate effective results.

Research objective

To date, the Big four firms have invested substantial capital in researching and developing large language models. To illustrate, KPMG and Deloitte have committed to investing $2 billion in AI-related services, while EY and PwC have committed $1.4 billion and $1 billion respectively.

According to a PwC survey ‘The fearless future: 2025 Global AI Jobs Barometer’, these investments represent an effort to contribute to the $15.7 trillion estimated economic impact of AI to the economy by 2030. These investments suggest that the Big Four firms project optimistic benefits for AI adoption. However, these large investments create numerous risks for the firms to consider when introducing this new technology.

In this article, a risk and benefit analysis will be discussed to address the adoption of AI in the accounting profession. To maximise the benefits and incorporate risks, accounting professionals should consider a responsible AI policy that covers many factors. To help generate a stepwise framework, interviews were conducted with three professionals in industries related to AI.

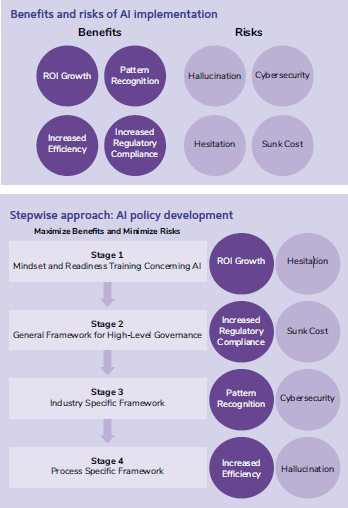

The benefits and risks chart below displays a summary of the benefits and risks of AI implementation for the accounting profession.

Responsible AI policy approach

A responsible AI framework would enhance the benefits of the technology, while also considering the associated risks. High-level governance frameworks exist at Big Four accounting firms. However, there is no one-size-fits-all solution, and a series of customised frameworks are needed to properly integrate AI into the profession. This can be established by creating frameworks for AI in tiered steps, with each step guiding employees in more specific measures.

The Stepwise approach diagram above displays a stepwise approach to AI policy development:

Each step will be described below, with each risk and benefit of progressing to the next step. When moving from earlier to later steps, more benefits are maximised and a greater number of risks are controlled.

Each step will be described below, with each risk and benefit of progressing to the next step. When moving from earlier to later steps, more benefits are maximised and a greater number of risks are controlled.

Stage 1: Mindset and readiness training concerning AI

The initial stage for AI training includes general mindset and readiness training to integrate the technology into the organisational culture. If employees are unfamiliar with AI, this programme would educate employees on the general uses of the higher-level features of the technology.

According to the Harvard Business Review, a framework for initial AI training may include:

Training simulations would be completed in a secure environment to allow employees to experiment with the technology.

As a result of this mindset and readiness training, ROI growth will be maximised as organisations begin to see a change in employee behaviour concerning AI adoption. Additionally, hesitation risk will be minimised as employees grow in comfort and confidence with AI technologies. For example, a manager at an accounting firm who is hesitant about staff workers utilising the tool may be less concerned with proper AI training provided.

According to John Blackmon, the chief AI officer of the custom training organisation at ELB Learning, employees may use the tool regardless of whether proper training or approval from management is received. Therefore, properly educating employees on procedures will ensure that AI is responsibly integrated into an organisation’s culture.

Stage 2: General framework for high-level governance

After enhancing employee readiness, Stage 2 involves creating a general framework for high‑level governance. According to Deloitte, an effective governance framework will allow firms to have a large governance structure to align people, processes, and technology. These frameworks will guide employees in ethical decision-making and state general policies.

A high-level governance framework maximises regulatory compliance as specific values can be linked to AI usage. As the regulatory environment is ever-adapting, this framework ensures that proper ethics are followed.

According to the Wall Street Journal, players in the financial services industry devote a considerable amount of resources to comply with new rules and policies. A general governance framework would encourage the ethical use of AI to comply with these various regulations, therefore increasing compliance.

Additionally, AI is developing at various speeds throughout the world, emphasising the need to address regionally focused frameworks. For example, the emergence of DeepSeek has alluded to AI development differences throughout the world. International organisations must understand the risks associated with the regions in which they operate to adequately communicate protocols to employees. Moreover, this framework minimises sunk cost risks that are associated with AI development.

Providing employees with proper ethical policies will enable them to responsibly use the tool, maximising the investments.

Stage 3: Industry specific framework

In Stage 3, an industry-level distinction should be made as the earlier frameworks can be generalised across firms. Similar to industry policies that employees can reference, a framework including specific AI applications for different industries would be provided. For example, a framework may be developed considering AI in the estimation of life insurance claims. In contrast, an entirely different framework for manufacturing clients or organisations may include using AI for inventory valuation methods.

These frameworks will allow employees to detect patterns as specific industry scenarios would be detailed within the framework. For example, a framework for car dealers may include historical industry trends to reference that the employee can utilise. Additionally, this framework may guide the employee to perform predictive analyses based on customer demands.

In terms of risks, cybersecurity concerns could be mitigated by protecting proprietary data and building in-house AI applications paired with access controls.

Stage 4: Process specific framework

The final stage that organisations should enact includes process-specific frameworks. Similar to the previous stage, Stage 4 would include multiple AI frameworks detailing different processes that an accountant would encounter.

According to Forbes and a Broadridge study, while financial service firms are investing heavily in AI, a majority of organisations do not have specific strategies in place to upskill employees. This framework would provide the greatest level of upskilling for employees to complete a specific process.

For example, to perform an inventory counting process as an accounting firm, the framework may suggest utilising drones to count inventory in a warehouse. The framework would explain how an auditor would test this process, ensure that proper controls were in place, and accurately document the usage of AI. The auditor conducting this procedure would maintain comfort, while senior staff would be able to accurately review the documented process.

This framework would maximise all of the discussed benefits and minimise all of the discussed risks, as accountants would be provided with detailed guidance in areas of ambiguity. In this framework, firms would realise the maximum level of efficiency as employees can adequately utilise AI as an assistant. The framework would guide employees to delegate tasks to AI technology in daily workflows.

Additionally, hallucination risk can be mitigated with proper prompt engineering, and this framework would guide employees to interact with the technology in specific tasks. Developing these process-specific frameworks would be time-consuming and potentially costly, but it provides the greatest positive impact for firms.

Conclusion

As accounting professionals are preparing for this technology, they must take the necessary steps to equip their employees with proper frameworks to reference in ethical or situational dilemmas.

Our responsible AI stepwise approach maximises benefits and minimises risks for the implementation of the technology. This approach will require research and capital by the organisations but will be necessary to properly integrate AI into organisational culture.

Additionally, employees must be willing to cooperate with organisational policies and use the tool if prompted. If the organisational leaders are eager to create responsible frameworks and employees are willing to learn about the technology, the accounting profession will have properly executed its version of ‘warp speed’.

Author bio

Dr. Tim V. Eaton is an EY Teaching Scholar, Arthur Andersen Alumni Professor, Professor of Accountancy, Farmer School of Business, Miami University

Dr James Zhang, Associate Professor, Accountancy, Farmer School of Business, Miami University

Alexa Leach, Accountancy Major, Farmer School of Business, Miami University