Last updated: 10 Feb 2025 09:00 Posted in: AIA

In recent years, corporate reporting has evolved significantly, reflecting the ever changing landscape of global business practices. Among the most notable developments to have taken place in this area are:

As companies strive to meet these new standards, integrating financial and non-financial information is becoming increasingly critical, paving the way for more comprehensive and insightful corporate reporting. This convergence of financial and sustainability reporting will play a crucial role in fostering a greener and more responsible global economy.

It is therefore critical to understand these changes, especially as the development of linkage between financial and sustainability reporting gathers pace. In this article, we explore these developments in the presentation of financial statements and the evolving world of sustainability reporting.

Presentation of financial statements

The IASB issued IFRS 18 in April 2024, effective for annual reporting periods beginning on or after 1 January 2027, subject to local endorsement (such as the EU and the UK), if applicable. The standard replaces IAS 1 Presentation of Financial Statements in its entirety, as well as making some changes to IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors.

The changes in IFRS 18 focus on the presentation, disclosure and communication of financial performance. This will help companies to tell their story through their financial statements, giving investors better financial performance information at the same time as enhancing the comparability of financial statements.

The Standard introduces three broad changes:

A company’s net profit will not change as a result of the Standard. What will change is how they present their results in the income statement and how they disclose information in the notes.

The introduction of the three new categories for the income statement is particularly important. Although it initially appears to be simply a remapping, when you start to apply the new approach, you realise that it is more nuanced than this. It is therefore essential to perform a full assessment of the impact of the new categories.

So reporters should start assessing the impact of IFRS 18 as soon as possible. It might be necessary to overhaul certain general ledger accounts, in order to ensure easy access to the right information when applying the Standard.

Sustainability

Sustainability reporting is a way for companies to report on matters relating to environmental, social and governance factors arising from their day-to-day activities. It is of critical importance to corporate reporting in the 21st century because the largest suppliers of capital – the insurance companies and the pension funds – will no longer invest in any business that doesn’t have excellent green credentials.

In recent years, sustainability reporting has also gained traction because businesses themselves are recognising the importance of transparency in their practices. This increased focus on sustainability reporting is driven by a growing awareness of climate change, social responsibility and the need for ethical governance. Stakeholders, including investors, customers and regulators, are demanding more comprehensive and accurate disclosures on how companies are addressing these critical issues. As a result, sustainability reporting has evolved from a voluntary practice to a crucial component of corporate accountability and long-term success.

However, before we go into the detail on the latest developments, we must consider the question: ‘What are sustainability disclosures?’

Sustainability disclosures fundamentally aim to provide readers with two types of information:

The red meat industry: An example of how this information can impact sustainability risks.

The red meat industry produces 14.5% of global greenhouse gas emissions. This arises from deforestation both for grazing and for soya production for their fodder. Once they have eaten, cows famously produce a lot of methane, which is very bad for the ozone layer. There are also many gallons of water used in the production of meat, while slurry created on intense factory farms pollutes rivers. Socially, many people have moral objections to the way that animals are mistreated in the process of being ‘factory farmed’ and then slaughtered.

These environmental and social harms have an impact back onto the meat industry. Meat producers are fined for the slurry that washes off their farms into local rivers. Increasingly, consumers are turning away from red meat for both environmental and moral reasons. Just look at your local supermarket, where the number of dedicated aisles for meat products is decreasing in favour of meat-free products.

As accountants, we can see that the reduction in demand for meat-based products could lead to impairment of abattoirs and processing plants, as well as additional costs for R&D, in order to investigate meat alternatives. Ultimately, this could even affect the going concern status. This extreme example shows how important it can be to report on sustainability risks and impacts.

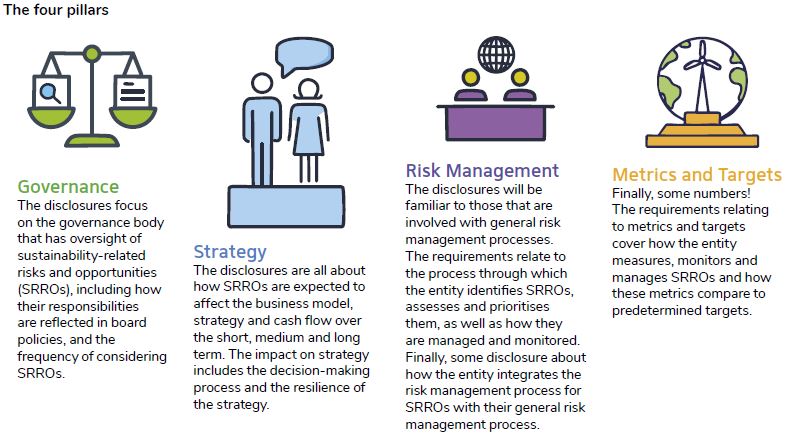

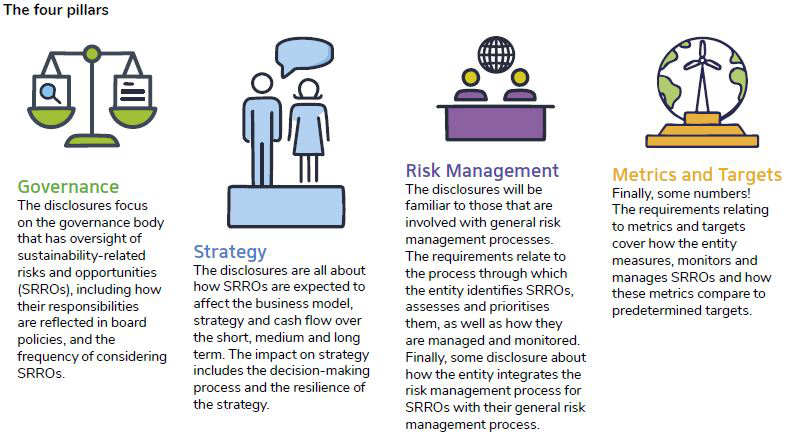

The most well-known sustainability disclosures – the ‘gold standard’, so to speak – are those based on the recommendations of the Task Force on Climate-Related Financial Disclosures (TCFD). The TCFD’s recommendations for disclosing climate-related matters created four pillars for disclosure: governance; strategy; risk management; and metrics and targets. These pillars have become the cornerstone of sustainability reporting.

Until recently, there were five well established organisations (and a number of lesser players), which had developed over the years, each with its own acronym and approach to sustainability reporting. The global reporting community felt this diversity was best remedied by mirroring the success of the IASB in relation to financial reporting standards, and called in the IFRS Foundation, with its extensive global network of users, to address the situation. The result was the formation of the ISSB in 2021. Its aim was to establish a single, authoritative, global baseline framework for sustainability reporting.

The ISSB

The IFRS Foundation, as part of establishing the new standard setter, brokered mergers between the five most established sustainability reporting organisations and the ISSB. This gave them a great base from which to develop Standards. They also decided to adopt TCFD’s well accepted approach, thereby engendering a high level of familiarity and acceptance from the reporting community.

The ISSB issued its first two Standards in June 2023.

Both Standards are effective for annual periods beginning on or after 1 January 2024, subject to local regulatory requirements.

See The four pillars for a high-level overview of the core content requirements. The core content applies to IFRS S1 and IFRS S2, with the only difference being that IFRS S1 refers to sustainability-related risks and opportunities (SRROs), whereas IFRS S2 refers to climate-related risks and opportunities (CRROs). Although the core content is the same, IFRS S2 provides much more detailed disclosure requirements needed for an entity to achieve the objective of each section as it relates to CRROs.

Materiality

At this point, you might think that we surely cannot disclose everything. That is entirely correct. The disclosure requirements relate to the significant items. The well-trodden concept of materiality comes to the rescue.

The ISSB standards introduce materiality similar to what we know and love in financial

reporting – sustainability-related financial information is material if omitting, misstating or obscuring that information could reasonably be expected to influence decisions of primary users. The primary users are investors, lenders and other creditors. This is called financial materiality.

The idea of double materiality has made its rounds. This is largely because of the European Sustainability Reporting Standards (ESRSs). The EU, rather than waiting for and adopting the IFRS Sustainability Standards, opted to develop their own framework. This culminated in publishing the ESRSs. There are currently two significant differences between the IFRS Sustainability Standards and the ESRSs:

Despite these differences, there has been tremendous work and progress to increase the usefulness and comparability of sustainability reporting in the past few years. The ISSB’s objective to provide a global baseline for sustainability reporting is now in sight.

As regulators all around the world debate the mandatory application of sustainability reporting, and other stakeholders increasingly demand such reporting, businesses that build the foundation of their own sustainability reporting at this early stage will certainly reap the benefits, most notably easy access to capital, of being a foresightful and engaged global citizen.

Author bio

Danielle Stewart OBE is a specialist financial reporting advisory partner at RSM, where she heads up the firm’s national service.

Tiaan Fourie is a director at RSM, focusing on corporate reporting – this includes sophisticated financial reporting, the evolving field of non-financial reporting, and their interlinking.