Last updated: 23 Mar 2026 10:00 Posted in:

The United Kingdom remains an attractive destination for American entrepreneurs and US-headed groups who are seeking access to skilled labour, a stable legal system and international markets. A shared language and broadly familiar corporate concepts often create a false sense of simplicity. In practice, the interaction between UK domestic tax law, US worldwide taxation and the US/UK income tax treaty produces a challenging compliance environment. Difficulties typically arise where legal structure, people and operational reality drift out of alignment.

For advisers working in this space, the recurring risks are rarely aggressive tax planning or artificial arrangements. Instead, they stem from routine commercial decisions – such as where directors perform their duties, how employees are engaged or how profits are extracted – which can quietly trigger permanent establishment exposure, controlled foreign corporation rules, payroll obligations or mismatched reporting.

Establishing a UK taxable presence

For a US individual or US company trading into the UK, the threshold question is whether UK activities give rise to a taxable presence. Under UK domestic law, a non-resident company is subject to corporation tax if it carries on a trade in the UK through a permanent establishment, as defined in Corporation Tax Act 2010 s 1141. This includes both a fixed place of business and a dependent agent who habitually exercises authority to conclude contracts.

Where a double tax treaty applies, domestic law is overridden to the extent the treaty is more restrictive. Under Article 7 of the US/UK Income Tax Convention, business profits are taxable only in the state of residence unless the enterprise carries on business in the other state through a permanent establishment. In that case, only the profits attributable to that permanent establishment may be taxed. Article 5 defines permanent establishment in a manner broadly aligned with the OECD Model. Preparatory or auxiliary activities are excluded, but fixed places of business and dependent agencies are expressly included.

In practice, HMRC places significant weight on substance. Permanent establishment arises under UK domestic rules as restricted by treaty protections. Once a permanent establishment exists, profits must be attributed on a separate enterprise, arm’s-length basis. Transfer pricing principles apply under Part 4 of the Taxation (International and Other Provisions) Act 2010.

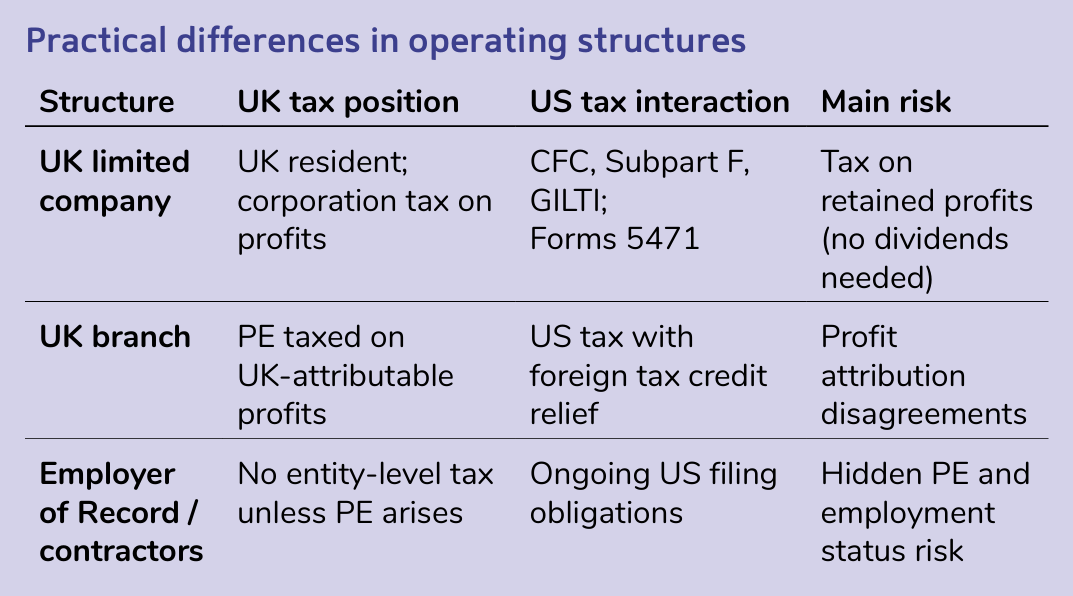

Choosing the right operating structure

Most US founders consider three initial routes into the UK market: forming a UK private limited company; operating through a UK branch of a US company; or engaging workers via contractual arrangements or as an Employer of Record while testing the market. Each option carries distinct tax, compliance and risk implications. The table summarises the practical differences most frequently encountered.

UK private limited company

A UK limited company is governed by the Companies Act 2006 and is tax resident in the UK by virtue of incorporation, subject to rare treaty tie-breaker outcomes. It is subject to UK corporation tax on its profits under the Corporation Tax Acts 2009 and 2010.

For financial years beginning on or after 1 April 2023, the main rate of corporation tax is 25% for companies with profits exceeding £250,000. A small profits rate of 19% applies below £50,000, with marginal relief available in between.

From a US tax perspective, a UK limited company owned more than 50% by US persons will usually be classified as a Controlled Foreign Corporation (CFC) under Internal Revenue Code sections 951 to 964. CFC and GILTI outcomes differ depending on shareholder type.

Although a UK corporation tax rate of 25% may allow access to the high-tax exception in some cases, this is not automatic. It depends on effective tax rate calculations, income characterisation and the shareholder profile. Individual shareholders often underestimate the impact of GILTI.

US reporting obligations also arise. For example, IRS Form 5471 or Form 5472 may be required to disclose ownership of the UK entity by a US company or US persons.

UK branch of a US corporation

A UK branch of a US corporation does not create a separate legal person but still it does create UK tax exposure. Once a permanent establishment exists, UK corporation tax applies to the profits attributable to the branch, calculated as if it were a distinct enterprise. Intra-entity charges – such as internal interest or management fees – are often restricted, which can increase the effective UK tax base.

In the US, branch profits remain taxable, with relief typically obtained through foreign tax credits under Internal Revenue Code section 901 and Article 24 of the treaty. Profit attribution disputes with HMRC are common in branch structures, particularly where functions and decision-making are split across jurisdictions.

Employer of Record and contractor models

Contractual arrangements and Employer of Record models can delay entity formation and simplify early-stage operations but do not eliminate risk. Where UK based individuals act in substance as dependent agents or operate from a fixed UK location, permanent establishment exposure may still arise, regardless of contractual labels. Similarly, the use of contractors does not remove employment or payroll risk if the underlying working relationship resembles employment in practice.

Employment, payroll and IR35 exposure

Hiring individuals in the UK creates immediate compliance obligations. Employers must operate Pay As You Earn (PAYE) under the Income Tax (Earnings and Pensions) Act 2003, withholding income tax and National Insurance contributions and reporting in real time to HMRC.

Employer Class 1 secondary National Insurance contributions are charged at 15% on earnings above the secondary threshold, subject to applicable zero-rate categories; Class 1A and Class 1B contributions are charged at 15%.

Where individuals are engaged through personal service companies or intermediaries, however, the off-payroll working rules, commonly referred to as IR35, must be considered. IR35 is a UK statutory regime; IRS worker classification is based on US common-law tests.

Employer of Record arrangements can simplify payroll administration but they do not override the underlying tax analysis. Under an Employer of Record model, IR35 does not apply.

VAT and indirect tax traps

Value Added Tax is often overlooked at the point of entry. A UK-established business must register for VAT once taxable turnover exceeds £90,000. By contrast, a non-UK-established business making taxable supplies in the UK is generally required to register from the first taxable supply, with no registration threshold.

This often catches US businesses early, particularly those providing digital services, consulting other cross-border supplies. Failure to register on time can result in assessments, penalties and denied input tax recovery. In practice, VAT compliance is often the first area of HMRC scrutiny for overseas businesses.

Cross-border mobility and management location

Individual mobility frequently creates unintended corporate and personal consequences. UK individual tax residence is determined under the Statutory Residence Test in Finance Act 2013. Once UK resident, individuals are subject to UK tax on worldwide income, subject to treaty relief and specific regimes.

The four-year foreign income and gains regime is elective and conditional. For directors and senior executives, duties performed in the UK are taxable as employment income under ITEPA 2003. More critically, the exercise of strategic control from the UK can shift corporate central management and control, with potential consequences for corporate residence.

From a US perspective, citizenship-based taxation under Internal Revenue Code section 1 continues regardless of residence, requiring careful coordination of foreign tax credits, treaty claims and payroll reporting.

Social Security and National Insurance contributions can often be aligned under the US/UK totalisation agreement, but relief requires formal certification and careful timing. Informal remote working arrangements frequently fail to meet these requirements.

Reporting, penalties and enforcement risk

Both HMRC and the IRS impose significant penalties for non-compliance. UK penalties for inaccuracies and failures are governed by the Finance Act 2007 Schedule 24, and escalate based on behaviour. In the US, penalties start at $10,000 per Form 5471 and $25,000 per Form 5472, per year.

With automatic exchange of information under FATCA and other regimes, inconsistencies between UK and US filings are increasingly easy for tax authorities to identify. For professional advisers, the reputational risk often outweighs the immediate tax cost.

Employment contracts and UK law alignment

When American companies begin employing staff in the UK, the employment contract itself becomes a compliance document rather than a simple HR formality. UK employment law is heavily statute-driven, and contractual terms must sit alongside mandatory rights under the Employment Rights Act 1996, the Working Time Regulations 1998 and the Equality Act 2010.

Unlike many US arrangements, UK contracts cannot contract out of statutory protections relating to unfair dismissal, notice periods, holiday entitlement or discrimination. Even senior executives benefit from these protections once qualifying conditions are met, and poorly drafted contracts frequently expose US employers to tribunal claims that would not arise under US law.

Conclusion

For Americans establishing businesses in the UK, success depends less on headline tax rates and more on aligning legal structure, people and operational reality across two systems that tax on different principles. The UK taxes based on residence, source and permanent establishment. The US taxes based on citizenship, ownership and anti-deferral rules.

The treaty mitigates double taxation but does not remove compliance or planning obligations. Early, coordinated advice that treats entity choice, employment models, VAT, transfer pricing and individual mobility as a single framework is essential. When alignment is achieved, the UK can serve as a robust, treaty-protected base for international growth. When it isn’t, businesses often discover that the cost of ‘simple’ decisions can compound quickly – and expensively.

Author bio

Simon Misiewicz

UK & US Cross-Border Specialist

Optimise Accountants

"For Americans establishing businesses in the UK, success depends less on headline tax rates and more on aligning legal structure, people and operational reality across two systems that tax on different principles."

Simon Misiewicz, UK & US Cross-Border Specialist, Optimise Accountants