This is the fifth annual public report detailing AIA's monitoring and supervisory activities in the United Kingdom and Republic of Ireland, covering the period between 6 April 2024 and 5 April 2025. The report demonstrates how we meet our regulatory requirements, combat economic crime, and support our members in fulfilling their obligations under the Money Laundering Regulations.

As a Professional Body Supervisor, AIA is dedicated to both enforcing compliance and educating members on their AML responsibilities. The information presented in this report highlights our regulatory efforts and the effectiveness of our AML monitoring and supervision activities.

In November 2024 AIA underwent a supervisory assessment from OPBAS as part of its annual monitoring activity. While we have achieved positive results and evidenced continued effective supervision, there is always room for improvement. We remain focused on enhancing AML compliance within our supervised population through targeted training, guidance, and robust monitoring and supervision.

AIA's Regulatory Oversight Committee continues to play a crucial role in ensuring our compliance with regulatory requirements and maintaining high standards of governance, providing independent scrutiny and oversight.

At the time of publication of this report the UK government has recently announced the outcome of its consultation into reform of the AML supervision framework. AIA is disappointed by the outcome of this consultation outlining the UK government’s intention to create a Single Professional Services Supervisor for AML.

We continue to believe strongly that moving away from professional body supervision of accountancy firms will not lead to more effective oversight. We are concerned that this shift risks significantly weakening the UK's efforts to tackle economic crime.

Professional bodies play a critical role in maintaining high standards, ensuring accountability, and fostering a culture of compliance within the accountancy sector. Their deep understanding of the profession and established mechanisms for supervision are essential components of robust and effective regulation. Transferring supervision to a SPSS risks losing improvements made by professional body supervisors working in partnership with the Office for Professional Body Supervision (OPBAS).

Although the timeline for implementation of this change is unclear due to the requirement to introduce primary legislation and make transitional arrangements, accountancy sector professional body supervisors remain an essential line of defence against illicit finance and economic crime.

AIA reaffirms its commitment to supervising its members in the public interest whilst continuing to support them in their critical role of preventing money laundering and combating economic crime.

In 2025-26, unless there are amendments to the planned supervisory reform we expect to be undertaking significant discussions with government and supporting a transition to a new supervisory model beginning with a consultation process in November 2025. This reflects our continued commitment to maintaining high standards of AML compliance and protecting the public interest.

George Josephakis, Chair, AIA Regulatory Oversight Committee

The goal of a large number of criminal acts is to generate a profit for the individual or group that carries out the act; criminals employ a range of techniques to clean their 'dirty money'.

Money laundering is the processing of these criminal proceeds to disguise their illegal origin and to make them appear legitimate, allowing criminals to enjoy these profits without jeopardising their source of income. Criminals do this by disguising the sources, changing the form, or moving the funds to a place where they are less likely to attract attention.

Illegal arms sales, smuggling, and the activities of organised crime, including for example drug trafficking and prostitution rings, can generate huge amounts of proceeds.

Money laundering is not only a crime itself, but also a key enabler of other serious crimes such as modern slavery, drugs trafficking, fraud, corruption, and even terrorism.

Professionals working in the accountancy, legal and property sectors are targeted because of their expert skills and services (National Risk Assessment 2025), which can give a cloak of legitimacy to illicit cash. This gives professionals a crucial role to play in protecting the UK’s economy, and wider society by reporting suspicious activity.

While money laundering isn’t always obvious, the consequences are severe. Even accidental involvement in money laundering could mean accountants losing their licence, receiving a fine, or facing criminal prosecution.

See more information on what money laundering is and key obligations for accountants.

Accountancy services are attractive to criminals due to the ability to use them to help their funds gain legitimacy and respectability, as implied by accountants' professionally qualified status. Those providing accountancy services remain at risk of being exploited or abused by criminals, especially if accountants become complacent in their regulatory obligations under the MLRs or willingly facilitate money laundering.

The accountancy services considered most at risk of exploitation include:

Most accountants work hard to prevent and spot money laundering and take necessary action, however some do unknowingly become involved. The key factors behind unwitting involvement continue to be failing to carry out proper due diligence and adequately train staff so they recognise and report potential money laundering concerns.

A very small number of accountants may knowingly cooperate with criminals to launder money.

AIA supervises its practising members for the purposes of the United Kingdom Money Laundering Regulations 2017 (as amended), where AIA is listed in schedule 1 as an approved supervisory body. In the Republic of Ireland AIA is a designated body under the Criminal Justice (Money Laundering and Terrorist Financing) Act.

Our work is overseen by HM Treasury, the Office for Professional Body AML Supervision (OPBAS) and the Republic of Ireland Departments of Finance and Justice.

We monitor our supervised population and take measures where necessary to ensure compliance, including:

We take appropriate measures to ensure we review:

We enforce the money laundering regulations and carry out our work as an AML supervisor through:

We work with other professional body supervisors, law enforcement, and regulators in the UK through:

We work with other professional body supervisors, law enforcement, and regulators in the ROI through:

The Regulatory Oversight Committee deals with scrutiny, oversight and review of the AIA's regulatory requirements as a recognised supervisory body under the Money Laundering Regulations.

The Committee is empowered to make recommendations to the Council to address areas of weakness or highlight areas of good practice relating to AIA’s AML supervision.

The Committee is made up of independent subject-matter experts. An extra layer of independent scrutiny provides added assurance and drawing on the broad experience of a range of industry professionals helps bring in new thinking from outside AIA.

Find out more on the work and terms of reference of the Committee.

The Regulatory Oversight Committee reports directly to AIA’s Council, which is AIA’s decision-making body responsible for ensuring we deliver the objectives outlined in our Constitution and meet our regulatory and statutory requirements.

AIA operates a risk-based approach to AML supervision. When applying for a practising certificate, applicants agree to co-operate with AIA with our Quality Assurance and Practice Monitoring process.

AIA's monitoring and supervision work ensures compliance with the AIA Constitution, Public Practice Regulations and legal and regulatory requirements including the Money Laundering Regulations.

The following tools are used to test members' compliance:

Where members are found to be non-compliant with the MLRs, depending on the impact and severity of non-compliance, an Action Plan is agreed to achieve compliance.

Where members exhibit serious non-compliance, act contrary to the AIA Constitution or fail to make adequate progress to achieve compliance, AIA undertakes regulatory action which includes the creation of an Action Plan and financial penalties. Failure to rectify deficiencies results in referral to AIA's Practice Compliance Committee and Disciplinary Committees which may sanction an individual or firm in line with the AIA Constitution and Sanctions Handbook using the following available options:

AIA's supervised population is made up of a subset of its overall Members in Practice population.

Some Members in Practice are supervised by other professional body supervisors (PBSs) where joint membership is held and this has been agreed with another PBS. AIA works with other members of the Accountancy AML Supervisors’ Group (AASG) to ensure all members are appropriately supervised.

As a professional body supervisor, we make sure that the relevant firms and individuals we supervise comply with the regulations and have appropriate controls in place to prevent money laundering.

In addition to providing pure accountancy services, a proportion of AIA supervised members undertake Trust or Company Service work. A Trust or Company Service Provider (TCSP) is any firm or sole practitioner whose business is to:

A person is still considered to be a TCSP provider even if these services are provided incidentally to other accountancy services, or they are provided infrequently or on a one-off basis.

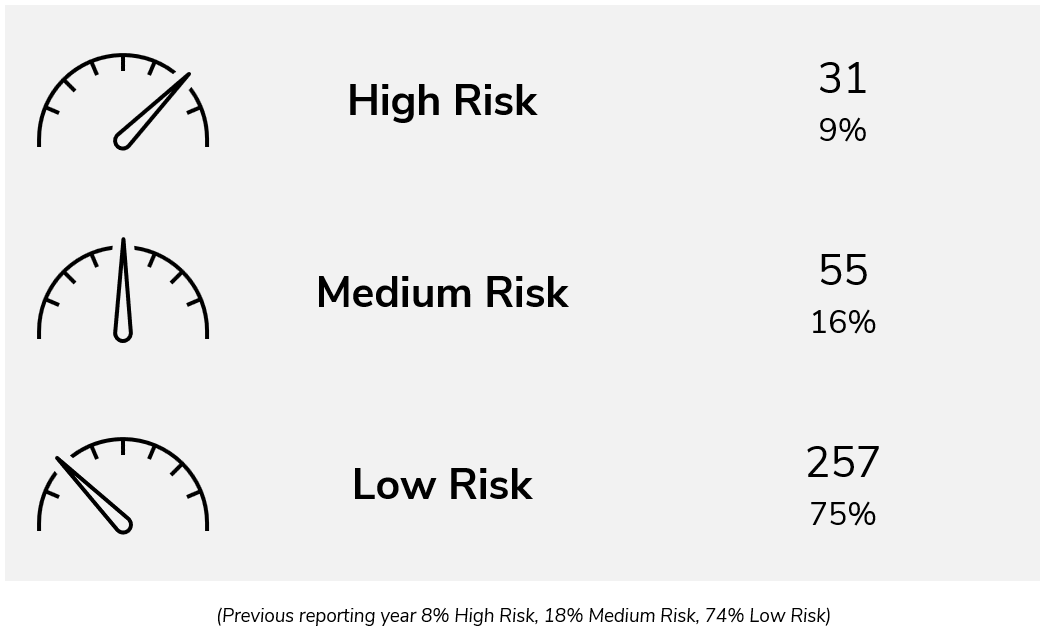

The money laundering regulations require that professional body supervisors create risk profiles for all regulated firms and individuals - High, Medium and Low. We use these profiles to identify money laundering risk and prioritise our monitoring and supervision.

Our risk-based approach methodology is controlled by a policy independently scrutinised by the Regulatory Oversight Committee and looks at a range of factors to determine risk, including regulatory history, size, clients and services provided. It also considers mitigation such as AML controls and compliance history.

We take monitoring and supervision action and review firms of all risk levels, prioritising higher-risk firms, as part of our risk-based approach.

Low AML risk does not mean no AML risk.

The MLRs require all beneficial owners, officers and managers (BOOMs) acting in an AIA supervised firm to be approved by us. They must get a Disclosure and Barring Service check and submit it to us when they first become a BOOM or take on a new role. This ensures that at the time of application the individual has no convictions for a 'relevant offence' as defined in Schedule 3 of the MLRs.

In the reporting period AIA authorised a total of 487 BOOMs (Previous reporting period: 452). This number fluctuates due to member retirements, disciplinary action or applications and depends how many BOOMs are present within individual firms.

52 applications for authorisation to act as a BOOM were received and 5 applications were rejected. 3 BOOM authorisations were invalidated by disciplinary measures.

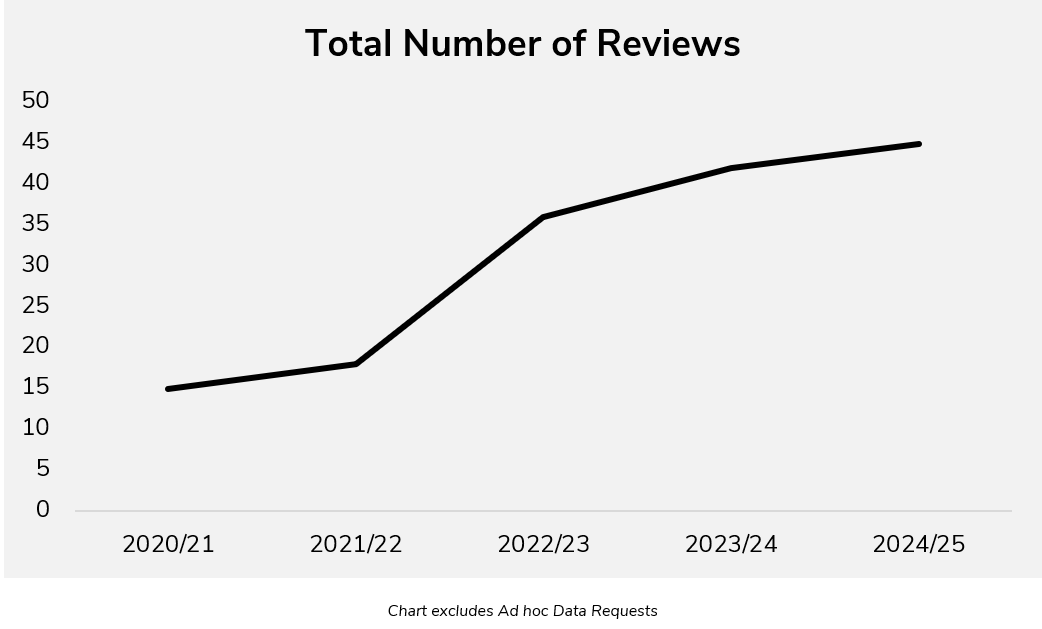

We undertook 45 Desktop Monitoring, AML Compliance Reviews, Onsite Monitoring Reviews or AML Online Questionnaires in the reporting period.

In addition, we undertook other targeted specific or ad hoc data requests.

The monitoring and supervision activity outlined above was conducted alongside thematic reviews, desk-based monitoring and individual requests made to members. For example, we worked with law enforcement agencies or made ad hoc data requests relating to members acting as verification agents for the Register of Overseas Entities.

AIA continues to investigate significant time and resources increasing the monitoring and supervision of members. Reviews conducted in 2024/25 represented 13% of firms receiving a Desktop Monitoring Visit, AML Compliance Review or Onsite Monitoring Visit. 5% of firms received an AML Online Questionnaire in the reporting year who had no previous monitoring or supervision review.

During a Desktop Monitoring, AML Compliance Review or Onsite Monitoring Visit we:

Through our AML Online Questionnaires we:

AIA operates a continuous improvement strategy to continue to deliver effective supervision. Improvements during the reporting period included:

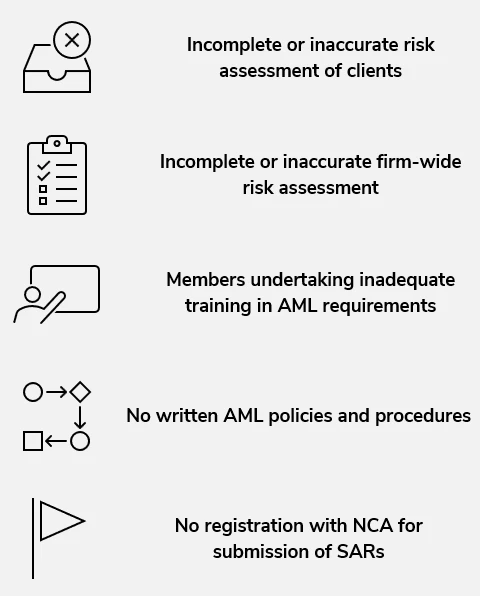

We have identified key risks within our supervised population include:

Our visits found the following levels of compliance with the MLRs among the supervised firms we reviewed as part of our monitoring and supervision activity. These figures relate to initial findings made in reviews prior to completion of any Action Plan of required or recommended actions provided to the member in a Findings Report:

Since 2023 we have collected enhanced data on the themes behind non-compliance at firms resulting from monitoring and supervision activity. In the reporting year themes included:

The most common forms of non-compliance with AML/CTF obligations identified throughout AIA’s supervisory activities include:

The most common form of non-compliance relates to inadequate documented policies and procedures. AIA has identified this as a focus for the next reporting year.

A common form of non-compliance identified during reviews is where members have failed to register with the National Crime Agency (NCA) to submit Suspicious Activity Reports on the NCA Portal. This is often because members feel they are not required to register until the moment they need to submit a SAR and that the frequency of SAR submission is low.

Following the monitoring and supervision action in the reporting period AIA undertook 41 informal actions (implementing an Action Plan for compliance for members and enforcing compliance) and 40 formal actions (including revoking practising certificates and excluding members). 9 members were excluded from membership.

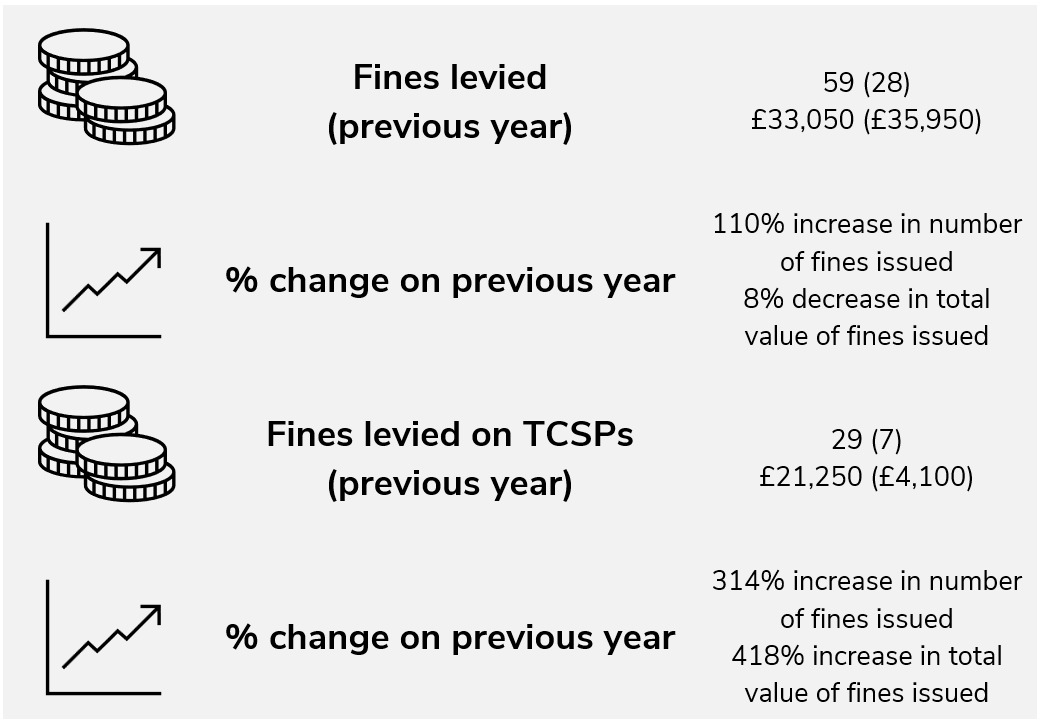

59 fines were levied in the reporting period totalling £33,050 (Previous reporting year: 28 fines, £35,950).

AIA issued a similar total of fines relating to AML non-compliance for firms providing solely accountancy-related work. This is due to the structure of AIA’s Sanctions Handbook which provides clear guidance for available monetary sanctions to disciplinary committees.

The figures reported above for TCSPs represent an increase in the number of fines levied and increase in the total value of fines levied.

These metrics are dependent on non-compliance identified remaining unrectified or fines issued by AIA’s Disciplinary Framework in line with the Sanctions Handbook. There is therefore no specific target number of fines or total amount of fines to be issued as this is a variable figure dependent on several factors.

Fixed Penalties

14 fixed penalty fines were issued (averaging £440) where members failed to correct areas of non-compliance within a deadline set by an action plan following a monitoring review.

For example, where a monitoring review identified that a member had failed to produce an adequate firm-wide risk assessment this would be noted on the Findings Report of the review and an Action Plan issued to the member with a deadline for providing evidence. Where a member fails to meet an initial deadline, a penalty is issued and the member must pay their fine and submit evidence as required in the original Action Plan by a new deadline to avoid referral to AIA’s Practice Compliance Committee.

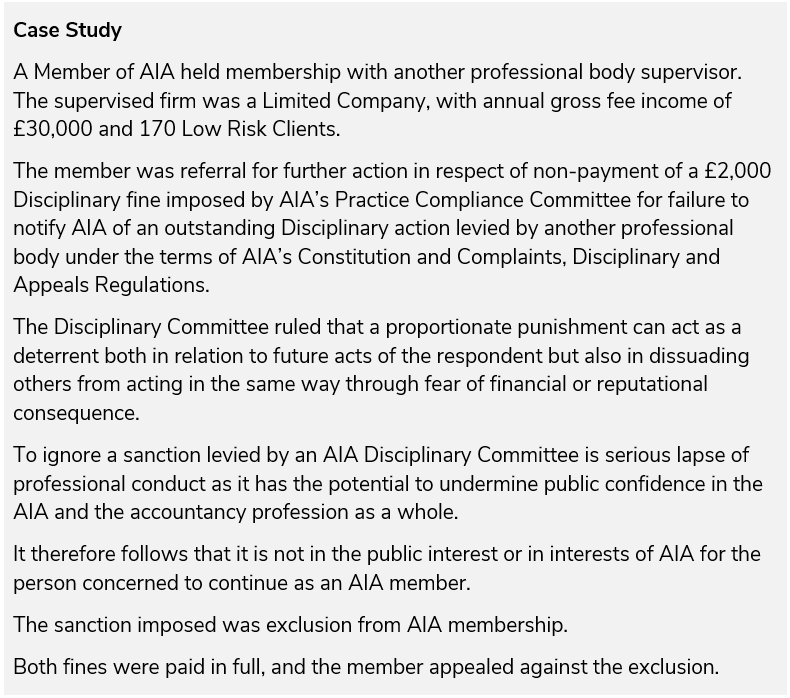

Feedback from members on our monitoring and supervision activity

Following each monitoring review AIA issues a feedback survey to members seeking views on how we can improve our process.

We have a dedicated money laundering reporting officer and deputy to meet our obligations to identify and report suspicions of money laundering.

AIA submits suspicious activity reports (SARs) to the National Crime Agency (NCA) if we identify a suspicion of money laundering through our monitoring and supervision.

To support this vital work, we regularly train and update all relevant staff and reviewers to recognise the red flags of money laundering and how to report them. We review the quality of SARs filed by our members during Onsite Monitoring Visits where records have been kept and make recommendations to aid improvement.

Where we see trends in criminal activity or suspicious activity in the course of our monitoring and supervision we work with other professional bodies through the Intelligence Sharing Expert Working Group (ISEWG) to issue alerts to the profession and set out appropriate indicators.

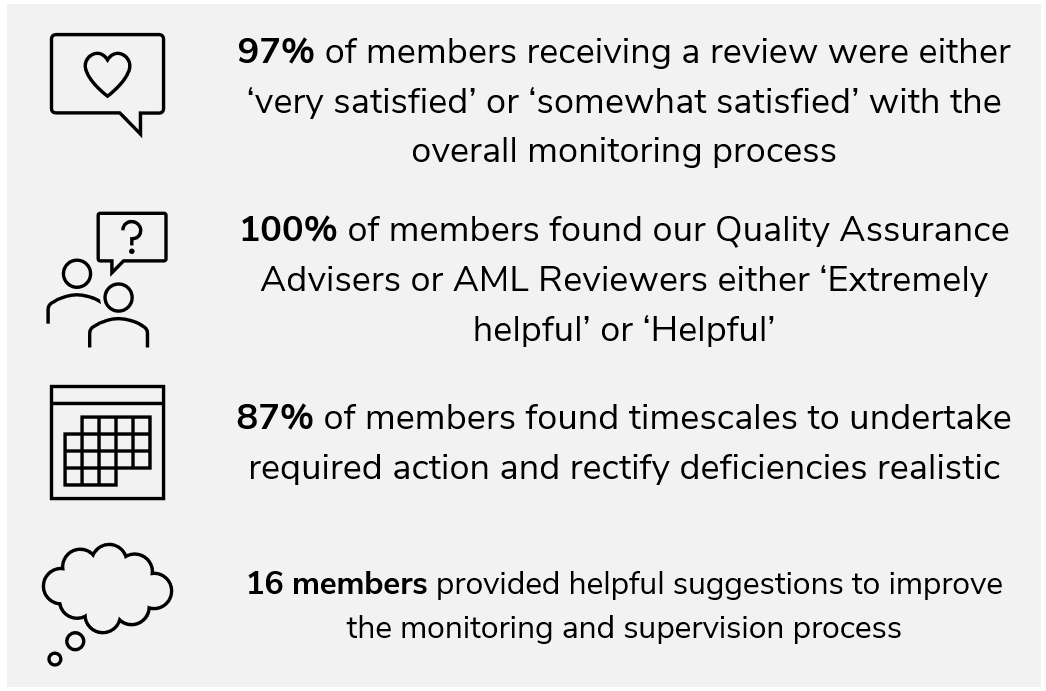

In January 2025 we issued our second public report on SARs reporting by AIA members, ‘Suspicious Activity Reporting Trends 2024-25’, detailing information on SARs submitted by AIA’s supervised population and their general categorisation to identify useful trends.

As part of the Annual Declaration AIA requires firms who have indicated a submission of a Suspicious Activity Report must explain, in general terms, the reason for their suspicion and report. The following themes linked to money laundering suspicion were identified during the 2024/25 renewal period:

AIA has a dedicated whistleblowing hotline and email address for money laundering disclosures.

This means we can be alerted by members of the public in a confidential way about occasions of non-compliance or potential involvement in money laundering or terrorist financing where AIA members are involved. No AML-related disclosures were received in the reporting year.

We remain committed to ensuring that these serious matters can be disclosed confidentially, and we have strict policies in place to maintain anonymity.

Anyone who wishes to make a confidential report about an AIA member or firm can do so if it is known or suspected that they:

If members of the public wish to report an individual or firm whose supervisor for AML purposes is AIA they can report the matter confidentially to our team.

Threats and emerging risks relating to money laundering and terrorist financing activity are changing constantly. Updated information is provided to AIA Members in Practice through a variety of channels to mitigate these risks.

AIA assesses emerging risks through a range of sources, including:

Where we receive information on emerging risks we provide structured alerts to AIA members to inform their training. AIA members are strongly recommended to read these alerts and take appropriate reporting action if they come across situations that involve the circumstances described.

To some extent during the reporting period the risks identified remained similar to those previously identified. We have seen a continued reliance on third-party client due diligence software to undertake client verification and due diligence. We would expect firms to be aware of the limits and risks associated with using third-party software and have issued guidance related to this risk.

The implementation of the Economic Crime and Corporate Transparency Act (ECCTA) and ACSP Registration is likely to continue to be relevant in terms of risk for AIA members.

At the time of publication of this report the UK government has recently announced the outcome of its consultation into reform of the AML supervision framework. AIA is disappointed by the outcome of this consultation outlining the UK government’s intention to create a Single Professional Services Supervisor for AML.

We continue to believe strongly that moving away from professional body supervision of accountancy firms will not lead to more effective oversight. We are concerned that this shift risks significantly weakening the UK's efforts to tackle economic crime.

Professional bodies play a critical role in maintaining high standards, ensuring accountability, and fostering a culture of compliance within the accountancy sector. Their deep understanding of the profession and established mechanisms for supervision are essential components of robust and effective regulation. Transferring supervision to a SPSS risks losing improvements made by professional body supervisors working in partnership with the Office for Professional Body Supervision (OPBAS).

Although the timeline for implementation of this change is unclear due to the requirement to introduce primary legislation and make transitional arrangements, accountancy sector professional body supervisors remain an essential line of defence against illicit finance and economic crime.

Building on the previous reporting period we consider that other current areas of emerging risk may continue to include:

Further information

AIA’s AML Sector Risk Assessment for Money Laundering and Terrorist Financing in the United Kingdom and the Republic of Ireland sets out information on money laundering and terrorist financing risk that is considered relevant to those individuals and firms supervised by AIA and informs AIA’s risk-based approach to supervision.

AIA’s sector risk assessment and risk-based approach has been developed considering guidance from the United Kingdom National Risk Assessment, the Republic of Ireland National Risk Assessment, the Financial Action Task Force Guidance for a Risk Based Approach for the Accounting Profession and updates from UK and EU authorities.

In the coming year AIA will continue to support supervised firms and members to help them put strong controls in place to prevent them from being used by criminals. This includes providing updated member guidance, CPD events, intelligence alerts and updating information on emerging risks.

We will also continue to take robust action where our firms and members are found to be failing to protect themselves and the wider public in their responsibilities under MLR.

We will continue to undertake an appropriate and effective risk-based approach to monitoring activity as we employ Onsite Monitoring Visits and leverage the flexibility of Desktop Monitoring Reviews and AML Online Questionnaires.

Trust or Company Service Providers (TCSPs) are considered as being at a higher risk of being used by criminals to facilitate money laundering in the National Risk Assessment 2025. We have worked with other professional body supervisors, HMRC, OPBAS and the National Economic Crime Centre (NECC) to develop our understanding of the threats, vulnerabilities and risks posed to our supervised population providing these high-risk services and will continue to keep our risk-based approach supervision under review.

Alongside our business as usual monitoring and supervision activity in the reporting period we:

In the coming year we intend to:

Member Survey

To support improvements in the effectiveness of AIA's supervision we conducted a survey of members to find out more about how our AML guidance is received.

Key findings:

Following the survey AIA has identified additional actions to improve understanding of money laundering risk and access to resources and will initiate a follow up survey in 2026 to assess results.

Published by AIA:

AIA maintains extensive AML guidance for members, including sensitive AML alerts and emerging risks, templates and checklists, and events, within the members' area of the website.

Examples of guidance we provide include:

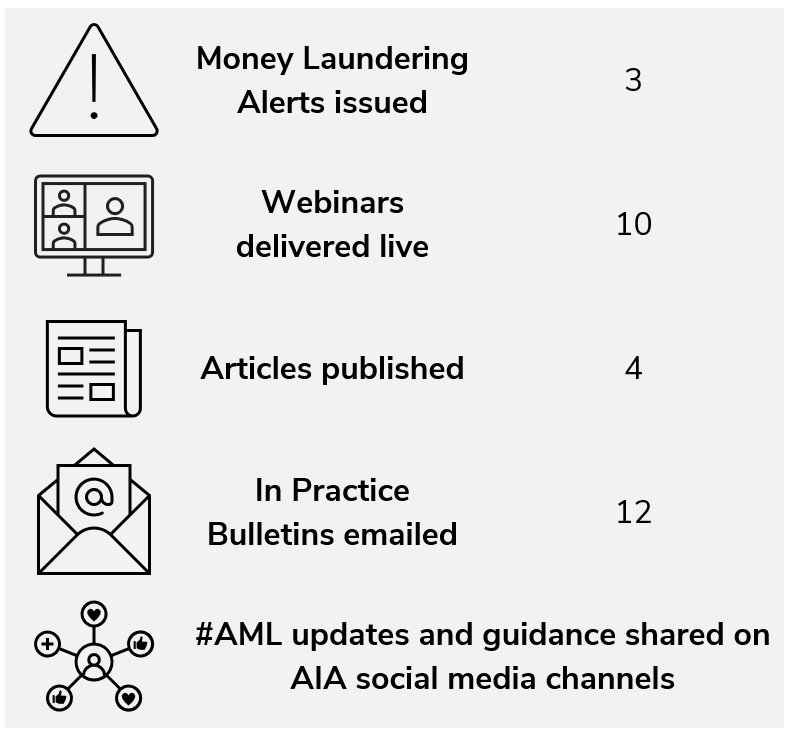

Regular AML updates are provided online to AIA Members who may watch recorded versions here. All past webinars are available for members on demand, including.

AIA maintains a library of AML-related articles for members to access on demand, for example:

Articles published in the reporting year include:

As part of an alerts sub-group of the Intelligence Sharing Expert Working Group (ISEWG) we issued 4 accountancy-specific money laundering alerts to Money Laundering Reporting Officers of our supervised firms and the wider sector:

Published by the National Crime Agency:

Published by Government:

Note: AIA’s responsibilities as a professional body supervisor under Schedule 1 of the Money Laundering Regulations 2017 involve the handling of sensitive intelligence and information which is used to combat the risk of money laundering and terrorist financing. This Annual Report does not include all aspects of AIA’s monitoring and supervision strategy and some information may not be disclosed to protect the public interest.